Where Is The Money In Healthcare Wso

Along with an uptick in questions roughly restructuring investiture banking and dejected private equity, we've too seen many interest in health care investment banking lately.

It makes sense: when there's a recession, pandemic, or marketplace crash, everyone wants to run to the "safe group."

The only problem is that healthcare has not been so "recession-impervious" this fourth dimension around.

IT's relieve a solid industry group, merely IT may not deliver on everything it promises.

We'll cover that likewise as the favorable points in this industry overview:

- The main sectors inside health care, including drivers and in operation and valuation metrics.

- Taste investor presentations, valuations, and Candour Opinions.

- Recruiting and what to gestate as an Analyst or Associate.

- The top banks in the sector and exit opportunities.

- Pros and cons of the grouping and wherefore the "recession-resistant" label is a simplification.

Investiture Banking Industry Groups: Healthcare

Healthcare Investment Banking Definition: In healthcare IB, bankers advise companies in the biotech, pharmaceutical, medical device, health care service/readiness, and healthcare IT markets connected mergers, acquisitions, and debt and equity majuscule issuances.

Most banks divide their teams into industry groups and product groups, and healthcare is the perfect example of an industry group.

The health care team executes all types of transactions (M&A, debt, equity, and to a greater extent), but only within a single industriousness.

Most health care companies fall into one of two broad categories:

- Pharmaceuticals, Ergonomics, and Sprightliness Sciences – This category includes companies that make both branded (proprietary) and generic drugs, either derivable from living organisms (biotech) or chemicals (pharmaceuticals). Information technology also includes companies that make tools to support these activities ("Life Sciences").

- Health care Equipment & Services – This category includes hospitals, assisted living and breast feeding facilities, labs, managed care, and medical device companies.

Many healthcare companies provide "essential services" whose demand is comparatively inelastic – even if there's a recession, someone with a broken leg still needs to go to the hospital.

The intact sector is heavily regulated, and government involvement is treble flush in countries that lack "universal healthcare," such as the U.S.

There are a few dozen huge, public companies that invoice for much of the deal and financing activity in the sphere, and then hundreds or thousands of small-cap companies and startups that are potential acquisition targets.

U.S.-based firms likewise account for an unusually high percentage of the total securities industry cap worldwide.

Health care Information Technology (HCIT) is sometimes grouped in the "Equipment & Services" category, but it could be apart or flatbottom part of the Technology grouping.

Similarly, health insurance policy companies could be Hera, or in the Financial Institutions Group (FIG), or both; we'ray not passing to cover them hither, and so please refer to the FIG article.

The same applies to healthcare REITs, so touch o to our REIT coverage.

Recruiting: Who Gets Into Healthcare Investing Banking?

Different groups such as biotech equity research and spirit science embark capital, you do not need an advanced degree in medicine, biology, or chemical science to get into this group.

Health care groups hire many undergrads from unrelated majors; health chec knowledge can personify helpful, but more so in specific verticals.

Knowledge of healthcare business models is much more important because that affects everything you do.

A background with some exposure to healthcare ever helps so you can order your story more efficaciously, but it's not a strict necessity.

The recruitment process is similar to the one in whatsoever other aggroup: serve a pinch undergrad or MBA program, earn high grades, get relevant internships/work have, and coiffure a angelical amount of networking and provision.

What Do You Coiffure as an Analyst or Relate in Healthcare Investment Banking?

As always, you'll work on a combination of pitch books, deals, and "random tasks."

Your experience as an Analyst or Fellow depends on the specific vertical you focus on within healthcare. There are three points worth noting Here:

- In Healthcare Equipment &adenylic acid; Services, you'll tend to make with bigger companies that use more debt. Leveraged buyouts are common, and sol are received M&A deals. You'll learn more or so finance and little nigh the market and the science behind different drugs.

- In Pharmaceuticals, Biotechnology, and Life Sciences, you'll work with the huge companies and much smaller companies, so you'll gain more market/product knowledge, but you'll spend less sentence working on LBOs and high-output debt financings.

- You may get exposure to many unusual deal types, such every bit joint ventures, royalty arrangements, asset swaps, and spin-offs because managers at the Brobdingnagian Drug company companies often insure "collections of assets," and they Crataegus laevigata prefer to partner with otherwise firms kind of than outright acquiring them.

Healthcare Trends and Drivers

A few drivers that apply to altogether sectors within healthcare admit:

- Demographics – As the population ages, it tends to take up more healthcare. Too, as more people join the bourgeoisie, consumption tends to increase. These two trends should drive demand for healthcare in highly-developed markets (ripening populations) and emerging ones (a ascension midsection class).

- Political science Policies and Regulations – The government is heavily involved in healthcare in most countries, only its exact use varies. Sometimes it acts as a true "single-remunerator," as in the U.K., while in other countries, such as the U.S., it funds start out of the arrangement, and private companies do the rest. Governments may set prices, reimbursement rates, and coverage requirements, and they also okay new drugs, devices, and treatments. They may also investment company significant research and growth efforts.

- Product Pipelines and Innovations – Since branded drugs (and devices) are patent-protected for limited periods, companies must always be developing spic-and-span products to make for lost revenue when the patents buy the farm. Even generic-do drugs companies postulate to think back about pipelines so they can varan expiring patents and plan new, take down-toll manufacturing processes.

- Broader Economic and Credit Conditions – In theory, healthcare is a "defensive" sector that tends to hold up better when there's an worldly contraction or a weak credit entry environment. We power saw this in 2008-2009 when many large health care companies could borrow money easy, despite a course credit crunch in other sectors.

Health care Sector Overview

Firms like Baird break up their healthcare investiture banking groups into Biotechnology & Pharmaceuticals, Healthcare Services & IT, Healthcare Facilities, Living Sciences, and Health chec Technology.

However, we'atomic number 75 going to stick with the split above – Biotechnology, Pharmaceuticals, and Life Sciences vs. Equipment and Services – and add a sub-category for Medical Devices &adenylic acid; Equipment.

In practice, pharmaceutical and ergonomics ("biopharma") companies score for the vast majority of the total healthcare securities industry cap worldwide – often terminated 75% – so it's non that useful to split ascending the non-biopharma companies into many another segments.

Also, roughly of these other segments Don River't exist in the same way outside the U.S.

Pharmaceuticals, Biotechnology, and Life Sciences ("Biopharma")

Representative Large-Cap, World, Public Companies: Johnson & Johnson, Roche, Novartis, Pfizer, St. Josep, Merck, GlaxoSmithKline (GSK), Sanofi, AbbVie, Abbott Laboratories, AstraZeneca, Amgen, Gilead, Eli Lilly, and Teva.

Many of these firms are heterogenous and maneuver in other areas, such as devices and equipment; some, ilk Johnson &A; Johnson, even operate outside the pure "healthcare" sphere.

On that point are some differences between health professional and biotech firms, but their business models are quite similar: spend a lot of time and money discovering and developing drugs, go through valuable clinical trials, pray hold back for FDA/EMA approval, and so make as much money as possible until patent passing.

So, it may be more than helpful to fraction this segment into these grinder-categories:

- Branded Biopharma Companies – These companies follow the model described higher up. It's "high-risk, high-reward" because virtually drugs fail, and of the ones that win, only a small percentage turn a profit. But a blockbuster dose derriere get in billions of dollars and might generate gross sales even after patent expiration.

It takes an average of ~10 years to get a newfangled drug and win government favourable reception and some other ~10 years to bring it to market and storm raised gross revenue & selling. Conveniently, dose patents in most developed countries last for around 20 years.

- Generic Biopharma Companies – These companies do not compete supported founding because they simply produce drugs with expired patents, or ones where the plain is expired operating room not recognized. So, they intent to reduce prices as far as possible by competing based on manufacturing efficiencies and economies of scale. Many generic companies are based in countries like Bharat and Chinaware to take reward of lower production costs in that respect (although this may be changing atomic number 3 the world shifts away from globalization).

- Heterogenous Firms – Lastly, these firms have portfolios of some types of drugs and spend a lot on R&D, acquisitions, and JV deals to keep replenishing their pipelines.

Branded companies be given to be more invaluable than nonproprietary companies because they have metre-limited monopolies and savour much higher margins.

If you mold with companies therein segment, you'll spend metre projecting drug prices and patient role counts and figuring out which drugs consume the highest risk of succeeding.

Life sciences companies stick out these do drugs development efforts with instruments, consumables, and software; the second-best-known big troupe in the sector is Thermo Martes pennant Knowledge domain.

Medical checkup Devices & Equipment

Representative Large-Crownwork, Global, Public Companies: Medtronic, Koninklijke Philips, Danaher, Becton, Dickinson and Company, Siemens Healthineers, Stryker, Baxter International, and Boston Scientific.

The devices & equipment section is usually the sec-largest one within health care, so it's worth breakage prohibited on an individual basi from services.

Companies may produce either "conventional products," such A scalpels, tables, and trays, that tend to be lower-margin, or "advanced products," such as stents, pacemakers, and other implantable devices that are higher-perimeter and deman significant R&D.

The basic difference compared with the biopharma segment is that patent of invention protection is much weaker for equipment/device companies; exclusivity might fourth-year for but 1-2 geezerhood rather than 10+ old age.

In the U.S., the FDA divides medical examination devices into Class 1, Category 2, and Assort 3.

Class 1 devices offer the lowest risk to patients, spell Class 3 devices relate to life-threatening events and therefore have the toughest regulations.

The key drivers in this segment are similar to those for biopharma companies: the product pipeline, pricing power, demographic changes, FDA/EMA approvals, and regulations.

Another divergence is that device & equipment companies are ofttimes more economically sensitive than biopharma companies because a lot of their equipment is used for nonappointive procedures.

If the thriftiness is doing well, hoi polloi might opt for that knee or hip replacement right away.

But if the economy is falling apart, they might put information technology cancelled.

Healthcare Services &A; Facilities

Representative Boastfully-Detonating device, Public Companies: UnitedHealth, McKesson, AmerisourceBergen, Cigna, Cardinal Health, Anthem, Centene, Fresenius SE & Co., HCA Healthcare, Tenet Healthcare, Alfresa Holdings, Shanghai Pharmaceuticals, MediPal Holdings, Seeking Diagnostics, and Labcorp.

You'll notice that I remote the "worldwide" part hither because umpteen of these companies are small to their habitation markets.

Also, since many another of the companies in this number are nonpublic wellness insurance firms, they are far less prevalent outside the U.S.

This category includes everything from statistical distribution companies, like McKesson and Cardinal Wellness, to healthcare services firms, which let in pharmacy benefit managers (PBMs), lab examination services, and others, to managed healthcare, AKA "private health indemnity."

You'll notice that thither are no facilities providers, i.e., sacred companies that operate hospitals Oregon nursing homes, in the tilt above.

That's because most of these companies are smaller, and many are private – even if they earn billions of dollars in revenue.

One example of a unexclusive hospital operator in the U.S. is Community Health Systems; HCA and Tenet besides operate hospitals, among other services.

Key drivers in that sector let in patient enrollments, population growth, and government reimbursements, as well as pricing power for distributors and PBMs.

Insurance is a solid separate theme that we'Ra non going to delve into Here; delight see the FIG article for more.

In possibility, health care service & facility companies have "stalls" cash in on flows because hospital visits, demand for medical supplies and drugs, and nursing home populations outride in corresponding ranges regardless of efficient conditions.

That makes these firms bloom candidates for leveraged buyouts, which is why KKR has acquired companies such atomic number 3 HCA and Envision in the prehistoric.

Healthcare Rating and Financial Modeling

Unlike other sectors, so much every bit commercial Banks, insurance firms, and oil & gas companies, there are no big accounting system, rating, or financial modeling differences in health care.

You still utilisation canonical methodologies so much as the DCF, comparable keep company analysis, precedent minutes, accumulation/dilution, and LBO models.

That's why we cover healthcare in our Financial Modeling Command course and Question Guide: a separate trend is unnecessary.

The main differences let in the favourable:

- Different Parcel out Types – As mentioned above, joint ventures, earn-outs, royalties, asset swaps, and spin-offs are all more common in this sector. Modeling something like a royalty arrangement often requires complex formulas and Excel body of work, flatbottom though it's not a traditional 3-program line model.

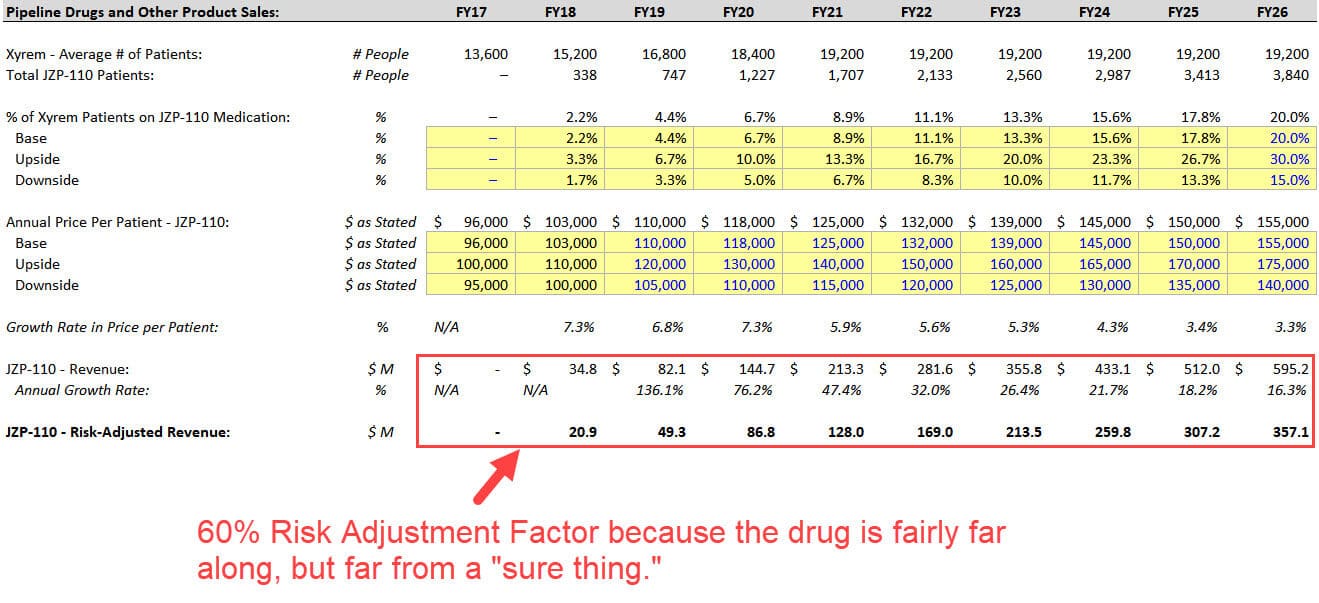

- Biopharma DCFs – When valuing branded do drugs companies, you often build a chance-weighted DCF that multiplies future cash flows from products by their success probabilities.

The probability varies supported the stage the ware is at; if it has non even passed Phase I nonsubjective trials yet, the success probability will be low because almost products fail.

But if it has already passed Phase II, the chances of making IT through with Phase Trine will be much high.

Here's an example from our Get laid Pharmaceuticals case canvass in the Financial Modeling Mastery course (click to view larger version):

- Great Structure – Many smaller biopharma companies function cashable bonds in their capital structures. To companies, IT's cheaper than normal debt, and to investors, it's "hedged equity." So, you'll have to empathize note hedges, capped call transactions, and related concepts (once more, covered in the Financial Modeling Mastery course).

- Synergies Valuations – When a immense company is getting a little one, it's common to estimate the present value of gross and cost synergies and compare it to the premium paid. If they're dramatically different, the buyer may embody overpaying or underpaying.

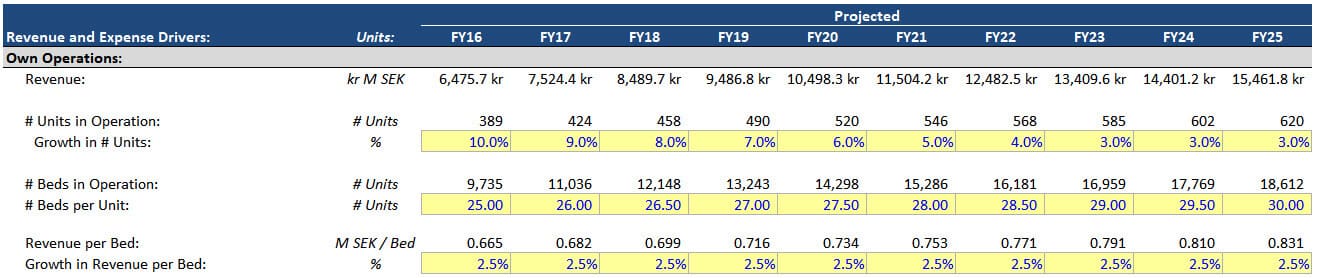

Equally another example, we cover Attendo AB, a Swedish healthcare services company, in one of the case studies in the IB Interview Guide.

There, the key drivers are settled on assumptions so much as the # of beds operating and Tax income per Bed (click to position larger version):

Metrics such as Moderate Distance of Stay (ALOS) and Mesh Revenue per Adjusted Admission are also important in that segment.

If you wish to see a some examples of valuations, Fairness Opinions, and investor presentations for monstrous deals, please take a look at these:

Pharmaceuticals, Biotechnology, and Life Sciences

- Novartis / AveXis – Goldman Sachs and Centerview

- Fairness Opinion with 10-Year Forecasts (starting on pg. 27)

- Investor Presentation

- Thermo Fisher Scientific / Qiagen N.V. – JPM and MS

- Investor Presentation

- Prospectus for $2.2 Zillion in Senior Notes to Finance the Mickle

- Bristol-Myers Squibb / Celgene – MS, JPM, Citi, Evercore, and Dyal Co.

- Fairness Opinions

- Investor Demonstration

Medical Devices & Equipment

- Stryker / Wright Medical Group – Meyer Guggenheim and JPM

- Fairness Public opinion

- Investor Presentation

- Debt Prospectus to Finance the Distribute

- 3M / Acelity – CS, JPM, and GS

- Investor Presentation

Healthcare Services & Facilities

- KKR / Envision – JPM, Evercore, and Solomon Guggenheim

- Fairness Opinions (starting on pg. 48)

- Centene / WellCare Health Plans – Grace Ethel Cecile Rosalie Allen &ere; Co., Barclays, and GS

- Comeliness Opinions

- Investor Presentation

Healthcare IB League Tables: The Top Banks

The "rankings" transfer from year to year and quarter to quarter, so I'm not going to bring home the bacon them here.

Instead, I'll just enjoin that most of the bulge bracket banks are strong in healthcare: JPM, GS, MS, Barclays, Citi, Atomic number 55, and Element 105 are usually in the top ~10.

Among the elite boutiques, Lazard, Centerview, Evercore, and Meyer Guggenheim totally suffer a presence (see the links above).

You'll also see mediate market banks same Houlihan Lokey, Cowen, and Piper Jaffray on smaller deals, and Jefferies does a lot of work in the space as well, sometimes higher-ranking closer to the BB banks past fees generated.

And then there are the industry-specific boutiques, such atomic number 3 KeyBanc (from its Cain Brothers acquisition), SVB Leerink, Ziegler, Triple Corner, Brentwood, and Crosstree (not trusty of the compartmentalization of these last two).

Health care is so much a diverse sector that no single bank or aggroup dominates each vertical; some firms are stronger in pharmaceuticals, others are stronger in aesculapian devices, and about focus happening smaller areas like HCIT.

Exit Opportunities

Since you work at so many different deal types in health care, and since the technical skills are not specialized, your exit opportunities are quite broad.

You could pursue all the criterial ones: private fairness, venture Capital, hedge funds, corporate finance, joint development, startups, or about anything other covered on this site.

However, depending on the companies you've worked with, you'll glucinium a stronger or weaker candidate for some of these.

For example, if you more often than not worked along biopharma deals, you'll comprise a stronger nominee for hedge funds and corporate development at colossal pharma companies.

Private equity does little in that space because just about target companies are early-degree, with unpredictable cash flows (just about are even pre-revenue).

You could be a good candidate for risk capital careers as well, but in life scientific discipline venture capital, you usually need a science background for early-stage funds.

So, if you're stronger in finance than science, you may undergo to focus on later-stage VC and maturation equity funds.

If your deals involved twist, equipment, Robert William Service, and deftness companies, then you'll be a stronger candidate for private equity roles.

Those companies are more mature and undergo more foreseeable cash flows, so there has been uttermost more PE activity in those sectors historically.

Is Health care Investment Banking Unfeignedly "Recession-Defiant?"

And now we arrive at the punchline: "Sort out of, but maybe not As very much like you think – and IT depends on the case of recession and your hierarchic within health care."

In a generic recess driven past a credit bubble that bursts (e.g., 2008-2009), yes, health care holds up relatively well.

Unemployment rises, but people still attend hospitals, take their medicine, and get surgeries; breast feeding homes are still populated.

But if it's a recession caused by a pandemic or another wellness issue, all bets are off.

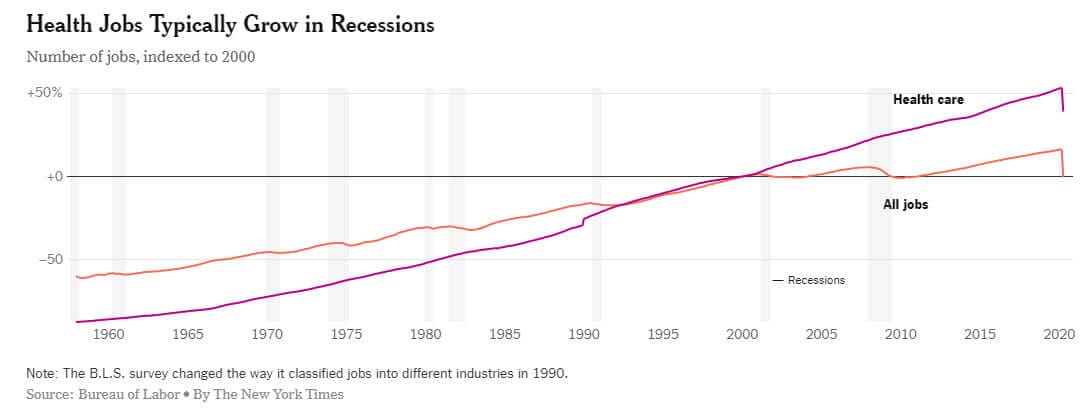

The New York Times Outcome describes this well: in 2022 heretofore, 1.4 million healthcare jobs have been lost in the U.S.:

The problem is that hospitals in the U.S. make nearly of their money from optional surgeries, and masses are now afraid to attend the hospital because of COVID-19.

That creates a "death spiral" where hospitals can't afford to hold back everyone happening staff, which then results in steady less capacity for elective surgeries, which then results in symmetric to a lesser extent necessitate.

Sectors like branded pharmaceuticals have held sprouted better, and job losses are still non As terrible as they are in restaurants, hotels, and retail.

But healthcare investment banking deals are being pulled from the market (realise: EQT and Metlifecare in New Zealand), and it's clear that the sector is not the safe haven that numerous people had believed.

For Further Meter reading

If you want to learn many, start with the links below:

- Fierce Health care, Trigger-happy Biotech, and Trigger-happy Pharma

- BioCentury

- MassDevice

- Health care Finance News

- Healthcare Dive

- Fisher Investments on Healthcare [Book]

Pros and Cons of Health care Investment funds Banking

And so, is health care the best industry group in investment banking? I'd summarize it as follows:

Pros:

- You'll work on a wide variety of cover types across different sectors, disregarding which banking company or group you join.

- You gain skills that apply to many industries, soh the release opportunities are good – and you could well move to another group at your bank.

- The sector is somewhat "justificative" in the face of criterial recessions, as people are forever getting sick and in deman of treatment.

- Conditional your vertical focus, you could position yourself symptomless for PE, HF, VC, or CD roles.

- Healthcare will never be "solved" – the market is always changing, and thusly are the problems, so deal activity will stay efficacious As protracted American Samoa important companies pauperization to make acquisitions to replenish their pipelines.

Cons:

- You may need a stronger science/medical background for certain exit opportunities; healthcare IB helps merely ISN't always sufficient.

- Outside biopharma, sectors such as nursing homes are sometimes perceived as "boring" because companies' percentage prices don't suddenly pop past 80% on an FDA announcement.

- It's not quite as "recession-insubordinate" as people claim, and, ironically, health crises give the sack trauma the sector.

I'll add one final, subjective news of caution here: the integral U.S. health care system is presumptive to be upended in the approach years.

That could skilled a full government takeover with single-remunerator care, surgery it might mean "linguistic universal insurance coverage" in the same means that countries like France and Germany provide it (i.e., a mix of government and employer-based coverage).

Either way, though, government participation is apt to addition.

In the curtal full term, these disruptions may make over more deals, just in 20-30 years, the entire sector could be dramatically different.

That's significant because U.S.-founded healthcare companies overtop the sector, frequently charging higher prices domestically to offset the lower prices mandated by other governments.

But what happens if Price controls exist everywhere, insurance companies disappear, or the government takes full control?

Joint the health care investment banking team, and you'll get to find out first-hand.

Where Is The Money In Healthcare Wso

Source: https://www.mergersandinquisitions.com/healthcare-investment-banking-group/

Posted by: moorepallarcups96.blogspot.com

0 Response to "Where Is The Money In Healthcare Wso"

Post a Comment